Data Science

Testing time-series stationarity in python

# -*- coding: utf-8 -*-

"""

Created on Tue Jun 29 13:51:56 2021

@author: Haderer

"""

import os

os.chdir(r"C:\Users\haderer\Desktop\ts")

cwd= os.getcwd()

print("Current working directory is:", cwd)

import pandas as pd

import pandas_datareader

from pandas_datareader import data

import seaborn as sns

from statsmodels.graphics.tsaplots import plot_acf

import numpy as np

from matplotlib import pyplot as plt

from matplotlib.dates import DateFormatter

from statsmodels.tsa.seasonal import seasonal_decompose

from statsmodels.tsa.arima_model import ARIMA

import matplotlib.pyplot as plt

df = pd.read_csv('msciemret.csv', parse_dates=['Date'])

df = df.replace(',','', regex=True)

df['Price'] = df['Price'].astype(float)

print(df['Price'].std())

# convert to datetime

df['Date']= pd.to_datetime(df['Date'], format='%b %y')

df.info()

df = df.set_index('Date')

df.sort_values(by=['Date'], inplace=True)

# Calculate the daily returns and log returns of price

df['Returns'] = df['Price'].pct_change()

df['log return'] = np.log(df['Price']).diff()

df = df.replace(',','', regex=True)

print(df)

df=df.dropna()

print(df.index)

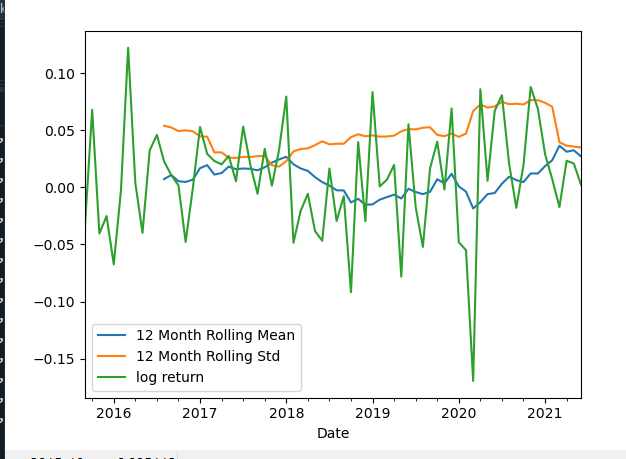

time_series=df['log return']

time_series.rolling(12).mean().plot(label='12 Month Rolling Mean')

time_series.rolling(12).std().plot(label='12 Month Rolling Std')

time_series.plot()

plt.legend()

decomp= seasonal_decompose(time_series)

decomp.plot()

from statsmodels.tsa.stattools import adfuller

def test_stationarity (timeseries):

#roling statistics

movingAverage = timeseries.rolling(window=12).mean()

movingSTD= timeseries.rolling(window=12).std()

orig= plt.plot(timeseries, color='blue',label='Original')

mean= plt.plot(movingAverage,color='red', label='Rolling Mean')

std= plt.plot(movingSTD, color='black', label= 'Rolling STD')

plt.legend(loc='best')

plt.show(block=False)

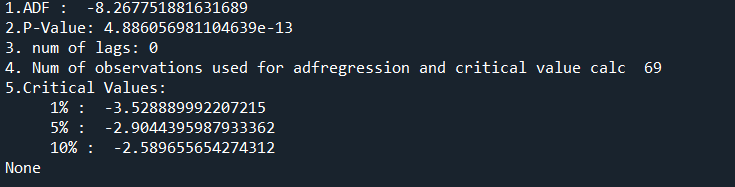

dftest = adfuller(df['log return'], autolag ='AIC')

print("1.ADF : ", dftest[0])

print("2.P-Value:",dftest[1])

print("3. num of lags:", dftest[2])

print("4. Num of observations used for adfregression and critical value calc ",dftest[3])

print("5.Critical Values:")

for key, val in dftest[4].items():

print("\t",key, ": ", val)

print(test_stationarity(df['log return']))

Portfolioflows

0