ARIMA Model with EM price data

Here is a simple example of an ARIMA model with pricing data. This is just an example to show the basic code used for ARIMA. Statistical tests in order to choose the appropriate model/lags are not included.

import os

os.chdir(r”C:\Users\haderer\Documents\python”)

cwd= os.getcwd()

print(“Current working directory is:”, cwd)

import numpy as np

import sys

np.set_printoptions(threshold=sys.maxsize)

import pandas as pd

from matplotlib import pyplot as plt

from statsmodels.tsa.stattools import adfuller

from statsmodels.tsa.seasonal import seasonal_decompose

from statsmodels.tsa.arima_model import ARIMA

from pandas.plotting import register_matplotlib_converters

register_matplotlib_converters()

df = pd.read_csv(‘msciemret.csv’, parse_dates=[‘Date’])

df = df.replace(‘,’,”, regex=True)

df[‘Price’] = df[‘Price’].astype(float)

print(df[‘Price’].std())

df[‘Date’]= pd.to_datetime(df[‘Date’], format=’%b %y’)

df.info()

df = df.set_index(‘Date’)

df.sort_values(by=[‘Date’], inplace=True)

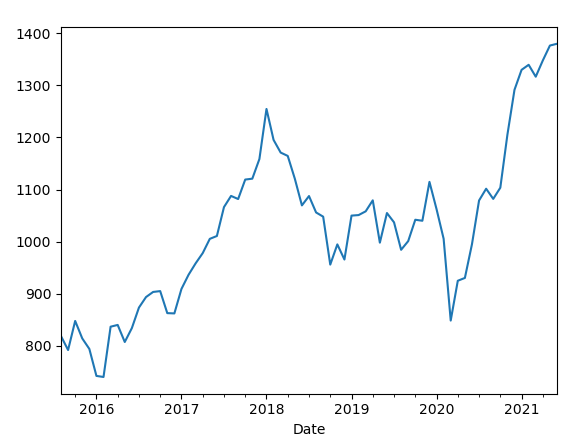

df[‘Price’].plot()

df_log = np.log(df[‘Price’])

plt.figure(2)

plt.plot(df_log)

plt.show()

df_log_shift = df_log – df_log.shift()

df_log_shift.dropna(inplace=True)

decomposition = seasonal_decompose(df_log)

model = ARIMA(df_log, order=(2,1,2))

results = model.fit(disp=-1)

plt.figure(3)

plt.plot(df_log_shift)

plt.plot(results.fittedvalues, color=’red’)

predictions_ARIMA_diff = pd.Series(results.fittedvalues, copy=True)

predictions_ARIMA_diff_cumsum = predictions_ARIMA_diff.cumsum()

predictions_ARIMA_log = pd.Series(df_log[0], index=df_log.index)

predictions_ARIMA_log = predictions_ARIMA_log.add(predictions_ARIMA_diff_cumsum, fill_value=0)

predictions_ARIMA = np.exp(predictions_ARIMA_log)

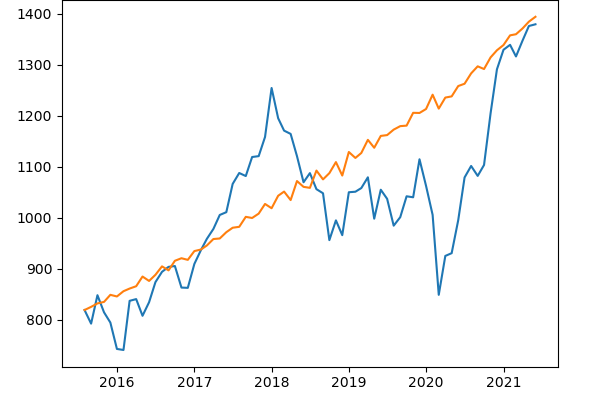

plt.figure(4)

plt.plot(df[‘Price’])

plt.plot(predictions_ARIMA)

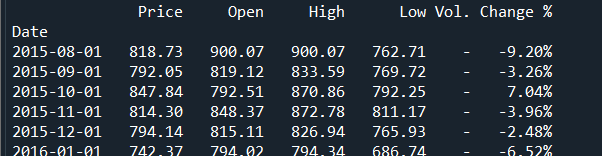

with pd.option_context(‘display.max_rows’, None, ‘display.max_columns’, None):

print(df)

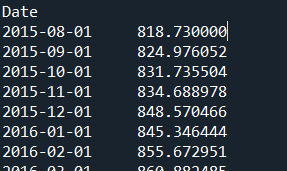

with pd.option_context(‘display.max_rows’, None, ‘display.max_columns’, None):

print(predictions_ARIMA)

RESULT:

s = predictions_ARIMA

df2=s.to_frame()

print(df2.head())

column_1 = df[‘Price’]

column_2 =df2.iloc[:,0]

correlation = column_1.corr(column_2)

print(correlation)

print(column_2)

print(column_2.describe())

print(correlation)

RESULT: 0.7501976605578393